http://www.accountingtoday.com

The Internal Revenue Service has issued the 2017 optional standard mileage rates to calculate the deductible costs of operating an automobile for business, charitable, medical or moving purposes.

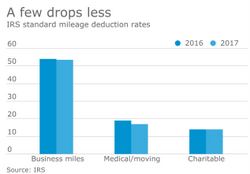

Beginning Jan. 1, standard mileage rates for the use of a car (also vans, pickups or panel trucks) will be:

• 53.5 cents per mile for business miles driven, down from 54 cents for 2016;

• 17 cents per mile driven for medical or moving purposes, down from 19 cents for 2016;

• 14 cents per mile driven in service of charitable organizations.

The business mileage rate decreased half a cent per mile and the medical and moving expense rates each dropped 2 cents per mile from 2016. The charitable rate is set by statute and remains unchanged.

“Factors contributing to the decision on this year’s slight decrease in the Safe Harbor reimbursement rate include declining fuel prices, which were largely offset by rising vehicle insurance and maintenance costs,” said Donna Koppensteiner, senior vice president of business development at Runzheimer, a business vehicle, relocation information and expense management services provider that provided data research and analytics to the IRS.

The standard mileage rate for business is based on an annual study of the fixed and variable costs of operating an automobile. The rate for medical and moving purposes is based on the variable costs.

The IRS reiterated that taxpayers always have the option of calculating the actual costs of using their vehicle rather than using the standard mileage rates. A taxpayer may not use the business standard mileage rate for a vehicle after using any depreciation method under the Modified Accelerated Cost recovery System (MACRS), or after claiming a Section 179 deduction for that vehicle. In addition, the business standard mileage rate cannot be used for more than four vehicles used simultaneously.

These and other requirements are in Rev. Proc. 2010-51. Notice 2016-79 contains the standard mileage rates, the amount a taxpayer must use in calculating reductions to basis for depreciation taken under the business standard mileage rate and the maximum standard automobile cost that a taxpayer may use in computing the allowance under a fixed and variable rate plan.

Be the first to comment on this post using the section below.