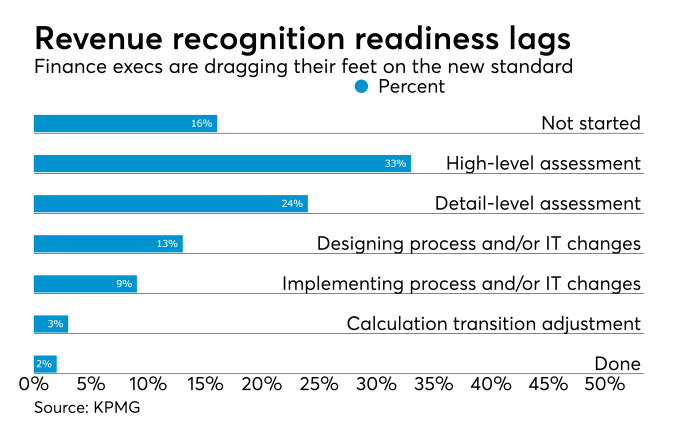

Relatively few public companies have been telling investors what impact they can expect to see from the revenue recognition accounting standard that takes effect next month, according to a new study from the CFA Institute.

The study is the third in a series from Vincent Papa, director of financial reporting policy at the CFA Institute, examining the upcoming standard. He and his colleagues examined the disclosures of early adopters of the new standard, including Microsoft, Alphabet, Raytheon, Ford Motor Company and General Dynamics.

“In several cases, the early adopters bring to the fore the effects on the amount, timing, and presentation of revenue attributable to key judgments in the new requirements,” he wrote. “Insight can also be drawn from the disclosure of impact by a few soon-to-adopt companies, such as British engine manufacturer Rolls-Royce. That said, investors and other readers of financial statements are by and large still faced with the challenge of discerning the effects and implications of these key changes to revenue reporting because of the fairly limited reporting, at an aggregate level, of either the realized or anticipated impacts of the new revenue recognition requirements.”

The ability of investors to understand the impact of the changes on their year-to-year revenue trends isn’t helped by the fact that many companies seem to be choosing the modified rather than the fully retrospective transition method, he noted. Companies are mainly providing fairly high-level and qualitative disclosures at this point, saying the changes will be mostly immaterial. But in reality, this could simply reflect the fact that companies have yet to fully understand the consequences of the changes, or it could be their claims of immateriality are misleading.

The study comes after Papa’s two 2016 white papers, Watching the “Top Line” and Top-Line Watch: Investor Considerations in the Run-Up to 2018. The new paper, Revenue Recognition: Key Judgments and Implementation Progress, reviews more key judgments, including those pertaining to sales with rights of return, gift card breakage, contract combinations and modifications.

“The first and second papers largely covered the implications of multiple-element arrangements, the principal agency issue, which has got a bearing on gross vs. net reporting, cost recognition, when you need to apply percentage of completion type reporting, largely shared by step number 5, and the disclosure requirements as well,” Papa told Accounting Today. “The latest one looks at the implementation progress, giving a sense of the extent to which there’s been early adoption as well as the levels of disclosure that have been provided.”

Papa pointed to a recent study by UBS, described in the CFA report. “It shows that in the main the majority of companies have not been able to fully disclose the anticipated effects of the new requirements,” said Papa. “There’s also been some analysis of the extent to which companies will choose one transition method vs. the other. In that respect, most companies are choosing the modified retrospective approach.”

That approach is not as helpful for investors, he pointed out. “For investors, you would hope for retrospective transition reporting because you would have more years of comparable data, and also some level of articulation of anticipated impact, particularly when you consider that traditionally revenue disclosures have not been as robust as is necessary. It’s quite hard for investors to perform on the basis of past disclosures without knowledge of company-specific contract profiles and the features of these company contracts. The disclosure of effects is crucial.”

One of the key judgments under the new standard pertains to variable revenue. “That’s one aspect of step 3, where companies need to estimate the transaction price,” said Papa. “In a sense they are left with conservative requirements. Under existing GAAP, there is need for revenue to be fixed and determinable. There tend to be more constraints around when or if companies can actually recognize revenue.”

He pointed to problems in judging what to do with loyalty points, gift cards and breakage.

“In the report, I mainly cover sales and right of return and gift card breakages,” said Papa. “There is some discussion around that, as implications. This is one area that can be quite pervasive. When you look at this area as it impacts retailers, gift cards are pervasive across many retailers, so it could be quite applicable to many sectors. It’s one aspect that’s clearly of interest.”

Loyalty points can affect the airline sector, but have similar issues as retailer gift cards. “Currently there is a diversity of approaches being undertaken,” said Papa. “Under the new requirements, conceptually there is a consistent approach, but it is more judgment intensive. We actually find for the airline industry, the level of deferred revenue could increase significantly. For example, in the case of loyalty points, there are two approaches. There is the cost accrual approach, whereby the deferral estimate would be based on the cost. Generally, costs tend to be relatively stable. For example, if there is a flight that’s given to me based on points without cost, you’ve got to estimate the market value of the flight, rather than the cost. One expects a higher magnitude of accruals being made and the deferred revenue being larger. That’s a case where the deferred revenue will increase.”

Many companies are being more conservative with how they account for gift cards. “With gift cards, currently some companies take a fairly conservative approach insofar as recognizing gift card breakage,” said Papa. “That’s gift cards that people don’t use; to wait until it’s nearly expired, then you recognize the breakage component. But under the new requirements, from day one you need to anticipate what portion will expire. There you will have a smaller component to gift card revenue. There will be an expediting of revenue. It can play both ways. It’s quite hard to generalize unless you look at it from a business model-specific, a company-specific standpoint.”

Software companies will also have to deal with when to recognize revenue from subscriptions and licenses.

CFA Institute recently did a webcast with officials from Microsoft and IBM discussing the issue. “The sense you got was that for was the pure-play software companies, those that are either pure-play cloud computing or mainly selling the license upfront, there won’t be much change,” said Papa. “But where you’ve got hybrid contracts, that’s really where changes are expected. As to whether the revenue is getting expedited or deferred based on the updated requirements, it’s hard to generalize. You really need to look at the company-specific level.”

The revenue recognition standard uses a five-step model:

1. Identify the contract or contracts.

2. Identify the separate performance obligations.

3. Determine the transaction price.

4. Allocate the transaction price to the separate performance obligations.

5. Recognize revenue when the entity satisfies a performance obligation.

Companies will need to give investors a better sense of where the judgments lie. “Even within a company there are multiple judgments, should there be five steps,” said Papa. “A company could have long-term contracts, and there’s a question of whether the percentage of completion type accounting will be at play or not. Then the extent to which you have to unbundle elements within contracts, that could be another factor at play.”

The more useful disclosures break down the key judgments and quantify them, according to Papa. “If you say just in a broad sense the changes are not material, what’s not really clear is whether there are offsetting effects. For it to be of predictive value in the long run, how is it going to translate into particular trends when you break it down by revenue type unless that breaks down almost by impacts by key line items as well as by key judgments? Then it’s less useful unless you’re providing that level of granularity within the disclosures.”

White Paper

Revenue recognition complexity simplified

Partner Insights

Sponsor Content From: