Critical audit matters are upon us, and the early results are in!

CAMs expand the independent auditors’ report to disclose audit-specific information that relates to accounts or disclosures that are material to the financial statements and involve challenging, subjective, or complex auditor judgment. The CAM requirements are contained in the Public Company Accounting Oversight Board’s standard, AS 3101, and are being phased in starting with audits of large accelerated filers for fiscal years ending on or after June 30, 2019. The CAM provisions of AS 3101 for other applicable filers take effect for fiscal years ending on or after Dec. 15, 2020.

Our firm, Kral Ussery, analyzed Form 10-Ks filed with the Securities and Exchange Commission for large accelerated filers with fiscal years ended June 30, 2019. Fifty such 10-Ks were identified, with 47 being filed in August and three during the first half of September 2019. The early results shed light on the types of matters being reported, as well as the average number of CAMs per audit report for the Big Four accounting firms.

Auditors disclosed from one to four CAMs for each of the 50 large accelerated filers, for a total of 89 CAMs with an average of 1.8 per audit report. Specifically, there were 22 with one, 19 with two, seven with three, and two with four CAMs.

The matters reported, and percentages of specific matters to the total of 89, are:

1. 27.0 percent: Goodwill and indefinite-lived intangible asset impairment (24) broken down as follows:

- Goodwill impairment (16)

- Combined matters of goodwill and indefinite-lived intangible asset impairment (7)

- Indefinite-lived intangible asset impairment (1)

2. 21.3 percent: Revenue recognition, four of which were specific to the adoption of ASC 606 (19)

3. 12.4 percent: Accounting for acquisitions, including the valuation of intangible assets (11)

4. 12.4 percent: Tax contingencies, including international assumptions and estimates (11)

5. 6.7 percent: Fair value of liabilities or equity (6)

6. 4.5 percent: Inventory valuation and reserves (4)

7. 3.4 percent: Allowance for loan and lease losses (3)

8. 3.4 percent: Capitalized software development costs (3)

9. 3.4 percent: Contingent liability judgments, including loss contingencies (3)

10. 2.2 percent: Related party identification (2)

11. 2.2 percent: Other management estimates and allowances (2)

12. 1.1 percent: Impairment of royalty interests (1)

Not surprisingly, nearly half of all CAMs related to goodwill and intangible asset impairment, and revenue recognition. Accounting for acquisitions and tax contingencies represented approximately a quarter of CAMS, with the last quarter being a mixed assortment of other valuation, estimates, allowances and judgmental matters. Even the two pertaining to related-party identification cited auditor judgment in assessing the sufficiency of the procedures performed to identify related parties and related party transactions.

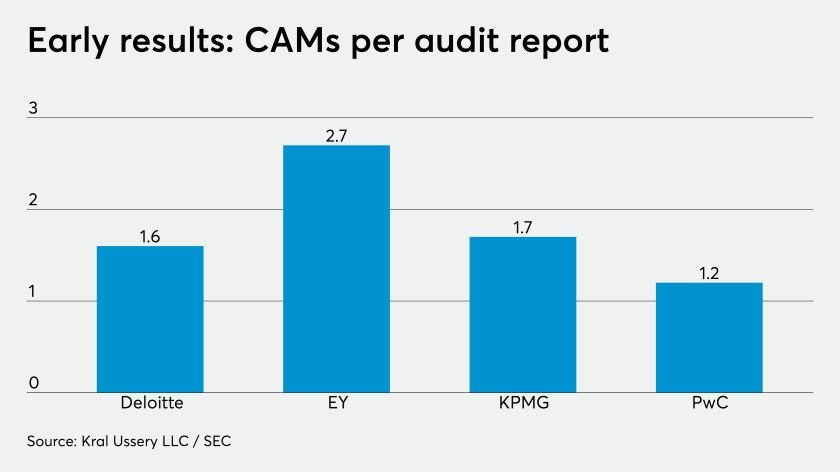

Perhaps the most interesting aspect of the analysis of these initial 50 audit reports with CAMs is the ratio of CAMs per audit report by Big Four audit firms. The following table conveys the results:

*Includes two audit reports by Crowe and Grant Thornton, and one audit report by BDO USA and Moss Adams.

As shown in the table, EY clearly has the highest ratio of CAMs per audit report at nearly three, while Deloitte and KPMG are near the average. PwC has the least with 1.2 CAMs per audit report.

We also noted that some of the CAM disclosures deviated from an example provided by the Center for Audit Quality in their publication “Lessons Learned, Questions to Consider, and an Illustrative Example,” in December 2018. In addition to adhering to the PCAOB’s AS 3101, audit firms are advised to keep the CAQ illustrative example in mind.

This early round of CAMs offers some insights and confirmations into the most challenging, subjective and complex judgments auditors face. Investors and other financial statement users now have a glimpse into the riskier areas of accounting and financial reporting through the eyes of the auditors. In addition, both public companies and other preparers can benefit in knowing where the most difficult audit areas are so they can steer effective controls in these directions.