The new lease accounting standard caused lease liabilities for the average company to increase 1,475 percent, skyrocketing from $4.4 million before the transition to $68.9 million post transition, as operating leases were recorded on the balance sheet for the first time, according to a new study.

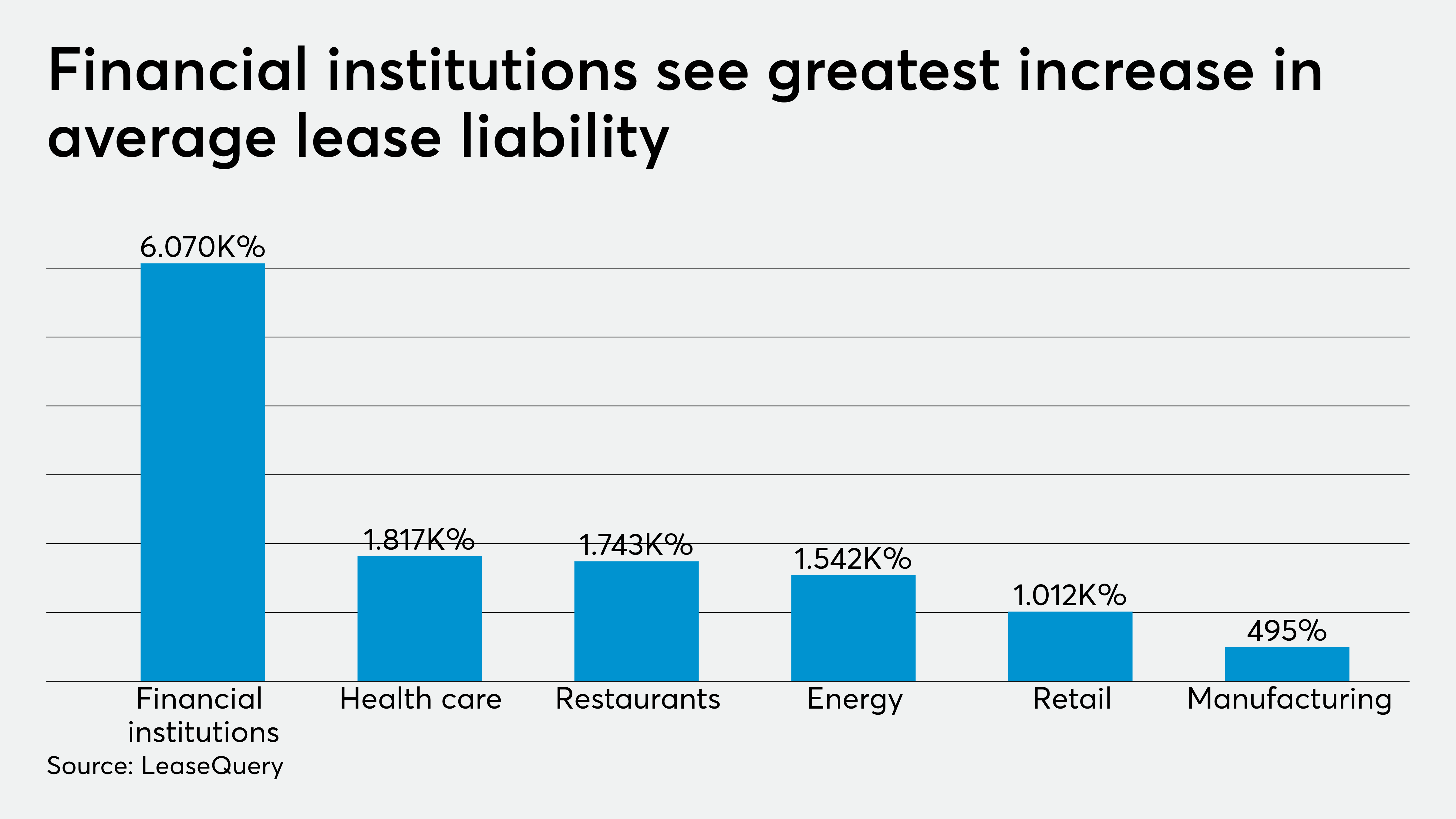

The study, from the lease accounting software provider LeaseQuery, analyzed more than 400 companies in its customer base and found that the increase was particularly striking in certain industries, such as financial services, where the amount of the average lease liability increased 6,070 percent. Similarly, in the health care industry, average lease liability liabilities went up 1,817 percent, in the restaurant industry 1,743 percent, in the energy industry 1,542 percent, in retail 1,012 percent, and in manufacturing 495 percent.

Initially only 37 percent of companies in the early transition to the new lease accounting standard thought it would be challenging, but 67 percent in the later stages of the transition reported difficulty. Companies have factored in only a year for transition, but many need much more time, and the Financial Accounting Standards Board is actually going to give private companies an extra year now to move to the new standard. Early steps recommended by LeaseQuery include understanding the accounting guidance, categorizing leases and testing software providers.

“All the public companies pretty much have decided that this is more comprehensive than they had expected,” said Jennifer Booth, vice president of accounting at LeaseQuery. “They first had to get this inventory of leases and figure out their lease population. Then they had to actually recognize the leases and determine the discount rate, so overall it’s been a bigger project than they had thought. The FASB heard from public companies and that’s why they gave the one-year delay [to private companies]. The FASB has even taken it a step further and they’re doing a roundtable at the beginning of April where they’re going to talk about the most complicated areas for public companies, such as the discount rate and embedded lease identification, to try to find a way, if possible, to make it potentially easier for private companies. I think that’s really an acknowledgement from the FASB that this was harder than we thought.”