Technology has a long history in the accounting profession. From the first abacus used by the Mesopotamians to today’s artificial intelligence and machine learning, every advance in technology has been met by accountants questioning how they will adapt to a new workplace.

A 2015 report from Accenture predicted “death by digital” by 2020, with 40 percent of transactional accounting work being automated. Now that the future is here, we thought it would be a good time to check in on that prediction. Has technology replaced the human factor?

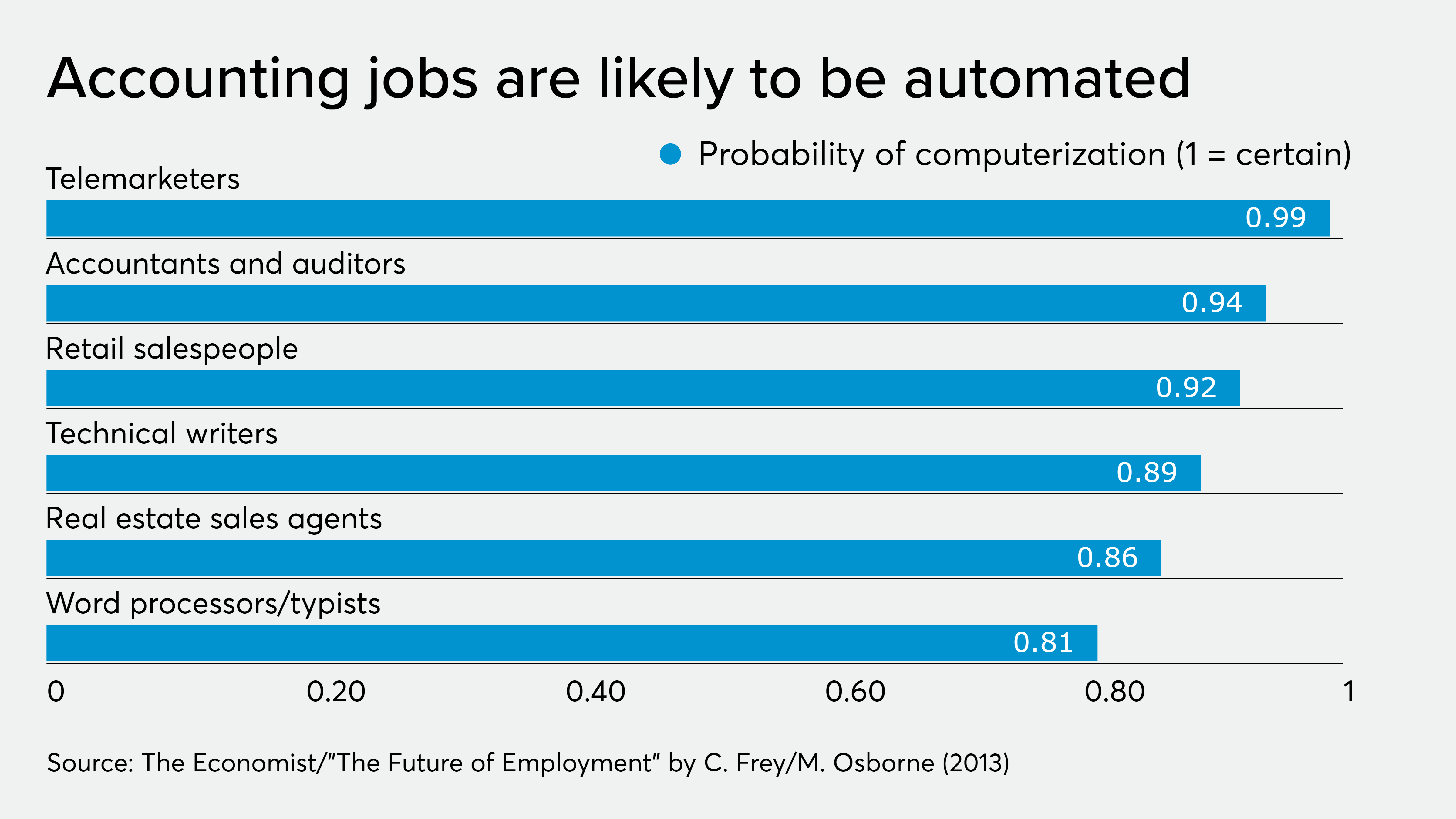

Technology and job anxiety

Emerging technologies such as artificial intelligence (AI) and robotic process automation (RPA) are changing the way work is done in every industry. The market size for RPA alone is expected to exceed $5 billion by 2024, according to a report from Global Market Insights, Inc.

In accounting and finance, companies are leveraging these technologies to increase efficiency and streamline business processes. But with these gains comes fear. In a 2019 survey by Robert Half, 12 percent of workers indicated automation would have a negative impact on their job by:

- Eventually eliminating their role;

- Reducing opportunities for creativity and problem-solving; and

- Forcing excessive reliance on technology to do their job.

However, even workers who believe technology will have a positive impact on jobs recognize AI and RPA will require them to develop new skills and processes.

Technology in the finance department

So far, automation in the finance department has been an opportunity rather than a job killer. It reduces cost and risk because computers make fewer mistakes and work faster. It has also served to shine a light on time wasted on low-value, repetitive tasks and poor processes.

Historically, many of the tasks accountants perform were built on manual data entry into legacy systems that didn’t integrate with each other. Think data entry, auditing a spreadsheet for errors, entering the same journal entry, or preparing the same reconciliation every month. Entire careers have been built on finding numbers, entering them in a certain spot, and performing routine calculations. But is that really the value accountants provide?

Technology and CPAs: A strategic partnership

The value of the finance and accounting team has never been its ability to count and crunch numbers. Rather, its power to analyze financial and operational results of the business and use those insights to drive better strategic decisions is where its value lies.

But humans are still needed to make logical and ethical decisions. So, technology is not eliminating jobs for CPAs, but liberating them to do the higher value work they were trained to do. And really, it couldn’t come at a better time, given the profession’s mounting workload.

The volume of data — with the same resources and accelerated due dates — that accountants must work with today is unprecedented and growing. Accounting teams are being asked to process increasing amounts of data and do more with the information they have. For those that are still using manual processes to do this work, the burden is tremendous.

Organizations already use financial and accounting software for account reconciliations, transaction matching, inter-company transactions, and resolving variances. Now, automation in the accounting and finance departments can help organizations improve the quality of their governance, reduce risk, deliver more insight, better manage working capital, and improve financial reporting by performing repetitive processes within the software.

Yair Holtzman of Anchin Block and Anchin has written in Accounting Today about the following three innovative technologies that are poised to impact accountants.

1. Big data analytics

Big data analytics studies large amounts of data to uncover hidden patterns, correlations, and other insights. A survey from the Institute of Management Accountants found that finance and accounting professionals are increasingly implementing big data in their business processes. Fifty-three percent of organizations are developing strategies around the use of big data, and 45 percent indicate their company takes a “strong” or “very strong” data-centric approach to information technology.

2. Blockchain

In recent years, blockchain technology has spread beyond its cryptocurrency roots. Initially a solution for governing transactions facilitated by cryptocurrency, blockchain technology, according to Harvard Business Review, “…is an open, distributed ledger that can record transactions between two parties efficiently and in a verifiable and permanent way.” It is being used in many industries, including health care, supply chain management, government, insurance, banking, and real estate.

According to Yair Holtzman, “Blockchain’s immutability as a general ledger makes it incredibly valuable to businesses. Information is not centrally stored by any business, organization, or governmental agency. The technology provides a quality audit trail as well as transparency of transactions, changes, or other actions along the business path.” This can significantly reduce an organization’s costs for annual audits as well as regulatory compliance.

3. Artificial intelligence

AI allows machines to perform tasks that typically require human intellect, including speech recognition, visual perception, decision-making, and translation. In an accounting department, AI helps accounting software learn to automatically perform analyses and draw conclusions: “Tasks like bank reconciliations, auditing expense submissions, and invoice categorization can be systematically automated,” Holtzman writes. AI can also be used for fraud detection by analyzing transactions to identify potentially fraudulent behavior.

Value of the human element

We can’t ignore the fact that the transactional level in an organization will shrink or disappear. Workers who spend their days on manual, repetitive processes like data entry and routine reconciliations will need to upskill — improve their existing skills and add new capabilities — and take on more strategic roles in the company to remain relevant.

But companies still need interpretation and judgment to realize the full potential of technology and automation. Rather than eliminate jobs, accounting and finance departments will need to shift their focus to developing more strategic and consultative initiatives within the company. Accountants who embrace technology can look for opportunities to apply their best skills and add value.

For most CPAs, technology won’t replace them. Instead, their roles will evolve and be augmented as they use technology as a powerful tool for their organization. Put it this way: The ways in which technology is, and will be, deployed in the accounting field will actually let CPAs do what they studied to do. Eventually, these emerging technologies will be so deeply embedded in finance and accounting that no one will talk about the software doing mundane work in the background. It will just be part of the daily routine.