With the new accounting standards weighing on companies that offer subscriptions as at least a portion of their businesses models, the first step is to admit there’s a problem.

The Financial Accounting Standards Board and the International Accounting Standards Board issued new standards — ASC 606 and IFRS 15 respectively — in 2014 for recognizing revenue from contracts with customers. The goal was to simplify and harmonize revenue recognition practices, which currently result in inconsistent accounting outputs for similar types of transactions. Beginning in fiscal 2018-2019, public and private companies of all sizes must adopt the new guidelines, which require recognizing an amount of revenue proportionate to the goods and services actually transferred to customers during the reporting period.

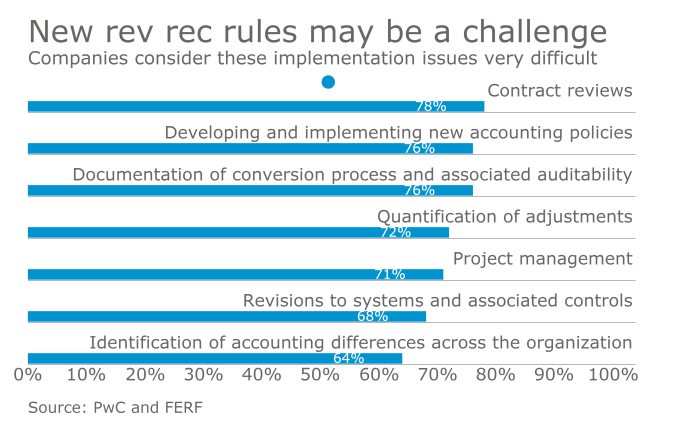

That isn’t easy.

The new accounting rules are considered by many to be the biggest change to accounting standards in the last 100 years. More than half the companies impacted, especially those bundling subscription and non-subscription services — that is, those with a “mixed business model” — are unprepared for it, according to PwC. Yet the number of companies with a mixed business model is growing every day. Established companies in media and entertainment, consumer services, telecom and utilities, financial services, health care, education, manufacturing and even farming are all adding subscription-based services, which are already increasing complexity for these companies, even without considering the new standards. The new standards serve only to increase the burden on corporate finance departments, especially those managing these complex calculations with spreadsheets.

Why are the new standards a challenge for subscription businesses?

First, subscriptions tend to change frequently. Whether from customer upgrades, downgrades or other modifications, contract changes are the norm. This can make something as simple as “identifying the contract” for compliance purposes a difficult proposition. In some circumstances, contract changes are mere modifications to the existing contracts, while in other situations, separate contracts are created — all with differing impacts on revenue recognition.

Subscriptions are also complex and rolled out over time, creating additional uncertainty related to handling common subscription characteristics, such as evergreen subscriptions and nonrefundable upfront fees — that is, whether to recognize the revenue right away or defer it. Similarly, usage-based pricing makes determining the transaction price difficult. All of this adds to the difficulty of accurately tracking contracted, recognized and unbilled deferred revenue. These challenges can in turn lead to inaccurate reporting, resulting in costly earnings restatements, tarnished reputations and even litigation.

And the new standards could limit new revenue opportunities for companies that avoid launching innovative and attractive new contract designs, pricing models and business practices for fear of falling out of compliance.

The New Standards in Action

The new standards are already creating a fair share of confusion as companies begin incorporating them into their reporting. Audit Analytics, a public company intelligence service, has found that some companies seemed to be struggling with ASC 606 adoption and predicts an increase in revenue recognition accounting failures. This isn’t surprising, as some companies seem to be benefiting from the new rules while others seem to be hurt by them.

For example, Aetna expects the new revenue recognition standard to increase its revenue and expense by $1.5 billion to $2.0 billion in 2018. SAP forecasts that IFRS 15 will add 200 million euros to profits. And Universal Technical Institute said its early adoption of the new accounting standard will result in a non-cash increase to equity of approximately $37.2 million as of October 1, 2018.

On the downside, GE’s stock tumbled after reporting that the adoption of new revenue recognition accounting standards would result in a non-cash charge to its Jan. 1, 2016 retained earnings balance of approximately $4.2 billion. The company will also recast its 2016 and 2017 earnings per share to reflect the change in accounting standards by lowering them by about $0.13 and $0.16. Rolls-Royce said adopting the new standard meant its core civil aerospace division took a £330 million loss last year, rather than the reported £520 million profit, and the company expects to remain unprofitable in 2018 on that basis.

What’s an Accounting Department to Do?

For subscription-only and mixed business model organizations, the first step in dealing with the new accounting standards is to admit the problem is serious and that inaction is unacceptable. In fact, there are several specific areas of the business model that need to be fully understood and tracked — and which are more complex now — to avoid significant reporting issues. These include discounts over a period of time, usage-based pricing, evergreen subscriptions, bundling multiple products together, ramp pricing, and mid-term price or scope change.

As a result, organizations will need to rethink and revise their current accounting practices to include elements and processes they have not previously had to consider. Since the costs and consequences of getting this wrong are so great — time-consuming restatements, damage to reputation, potential litigation — businesses should seek advice from a reliable third-party, such as a top audit firm, to determine the scope of the required changes and the best path forward.

The financial team must also educate itself about the new standards and develop the necessary skills to understand how future decisions regarding subscription strategies will impact revenue recognition. This is the only way to support innovative sales and marketing efforts without jeopardizing compliance.

Finally, depending on the scope of the changes required, CFOs will need to select a technology solution capable of keeping them in compliance with the new standards and the continually evolving financial landscape. Keep in mind, these new accounting standards are not the only challenge for finance teams. Evolving international trade regulations and tax reform policies will also have significant impact on the bottom line, business practices and valuation. The right foundational technology that can automate business processes and adapt to change is essential for long-term success.

White Paper

ASC 606 Compliance Requirements Made Easy

Partner Insights

Sponsor Content From: