Accounting professionals, as the stewards of financial information, have a unique opportunity to take the lead in adopting the new lease guidance and implementing lease accounting software. Approaching the adoption methodically, which includes collecting data, making policy decisions, and applying operational realities, accountants play a distinct role in developing the processes and implementing the systems that guide an organization into the future. In doing so, accountants can help companies capture the benefits of enhanced, centralized processes, improved lease management and increased data visibility that ultimately lead to cost savings and more accurate financial data and disclosures.

One of the keys to realizing these benefits is for accountants to embrace technology as part of the implementation process. Unlike cumbersome and error-prone spreadsheets, lease accounting software that is effectively implemented will allow accountants to efficiently analyze vast amounts of asset data and make informed decisions. Empowered by the centralized data from the lease accounting software, accounting professionals are positioned to add valuable insights on lease spend, advise on both operational and financial decisions and provide more in-depth and accurate financial analysis.

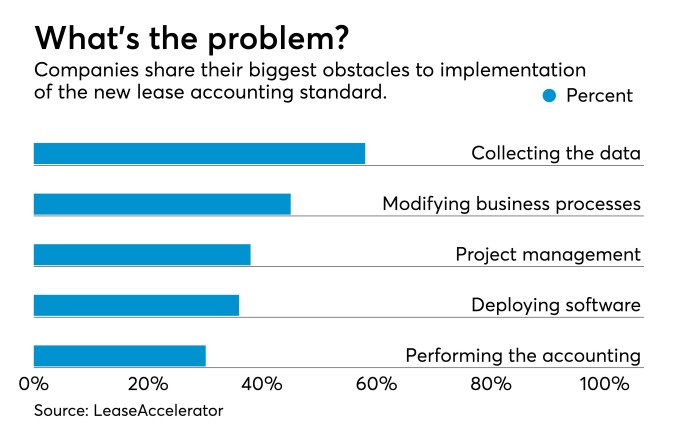

Selecting and implementing lease accounting software

Lease accounting software, when judiciously selected, enables accountants to help their organizations capitalize on streamlined data. At the highest level, the most appropriate solution will come from a financially stable vendor with lease experience and be SOC 1 compliant. When evaluating software options, understanding your company’s business requirements is critical. Specific items to consider include the lease portfolio characteristics, international reporting requirements and foreign currency translation needs. To cement the selection process, users need to be able to easily input data, navigate the modules, and produce disclosure reporting.

Beyond ensuring that a solution meets your company’s requirements, a system should be easy to implement. Employing a lease accounting system requires organizations, specifically accountants, to coordinate cross-departmental teams that will assess the current state and inform the development of future state processes around procurement, month-end close journal entries and asset management. Leading the implementation presents a strong opportunity for accountants to move beyond the numbers and partner with upstream functions that often do not understand how their processes impact financial information.

Enhanced, centralized processes

Creating more efficient, centralized processes to not only collect information but to accurately input data into a system will pay dividends. On the front end, by working with procurement and operations, accounting can implement processes that ensure compliance with the new standard. This approach paves the way for accountants to be the Center of Excellence and subject matter experts for advising both operational and financial decisions. For example, as part of a monthly or quarterly process, accountants can utilize a lease system to provide more timely and accurate analysis of lease spend, ultimately leading to cost savings and an improved bottom line.

Additionally, the new guidance has a significant impact to the financial statements and disclosures, requiring accountants to thoughtfully strengthen internal controls and improve reporting processes. For instance, lease information that previously resided only in the footnotes is now presented as a liability that will be subject to increased scrutiny from internal and external stakeholders. Through heightened attention and robust processes around lease terms and details of lease transactions, accountants can make certain the financial statements under the new guidance are accurate.

Improved lease management

Lease accounting software and centralized lease management allows accountants to monitor and make educated decisions on lease events. Typical events include amendments to add or remove assets, altering length of term and middle- or end-of-term options such as terminations or renewals. Specifically, with lease accounting software, companies can produce standardized and customized reports to assist in presenting actionable information. A common benefit to these operational reports are their assistance to inform decisions on whether to renew or end a lease agreement prior to the lease end date, ultimately reducing unwanted month-to-month lease expenses which may have previously gone unnoticed.

More complete and accessible lease data will position accountants to assist their companies with proactively managing assets. To illustrate, lease versus buy decisions may oftentimes be uninformed because of the lack of data and decentralized lease management, resulting in inefficiencies and overspending. The centralized monitoring of lease events will help inform lease versus buy strategies that produce efficiencies and cost savings related to common challenges like evergreen leases, vendor management for similar leases and end-of-term options such as lease extensions.

Increased data visibility

Cross-departmental collaboration and an effective lease accounting software implementation will lead to a more cohesive and efficient data flow. This improved workflow creates on-demand access into lease data and knowledge sharing between previously disconnected areas of an organization like purchasing, real estate, IT and accounting. Currently, accountants are often delayed in receiving information that could impact timely journal entries. In the case of leases, communication about a new contract may not occur until after the month closes, resulting in catch-up entries and the risk of misstatements in financial reporting. With a new lease accounting solution and efficient workflow, accounting groups will have visibility into upcoming and recently transacted agreements to influence management with concrete financial analysis on lease spend.

As accountants take leadership roles in the adoption of the new guidance and the system selection and implementation processes, companies will realize value from enhanced, centralized processes, more robust management of leases and more in-depth visibility to lease data. These improvements provide accountants with the opportunity to provide their companies with analysis and insights on critical capital-asset procurement and spending. Ultimately, successful adoption of the lease guidance will yield cross-departmental collaboration and efficiencies, more cost-effective lease decisions, and increased accuracy in financial reporting.