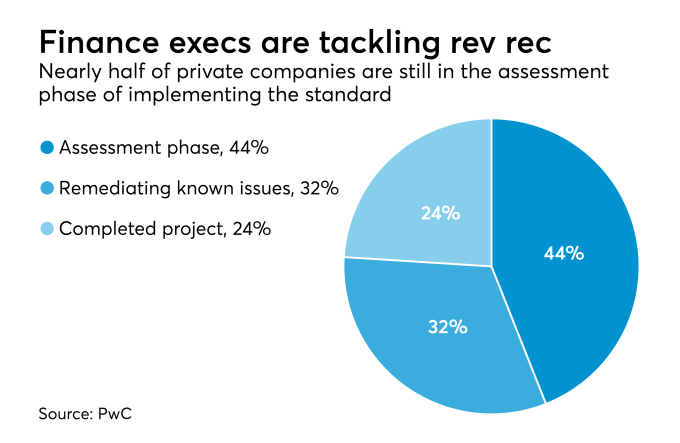

Now that public companies have begun complying with the new revenue recognition standard and private companies will need to implement it in the next few months, the underlying challenges are becoming more apparent in comment letters from the Securities and Exchange Commission.

“The majority of the comments that we’ve seen, both for the early adopters and then for the regular adopters that adopted it in 2018, primarily focused on performance obligations, which is not surprising,” said Rob Peters, senior director of customer experience and knowledge at Intelligize, a Reston, Virginia-based company that has developed a tool to help accountants track rule changes and determine market standard language for accounting policy disclosures. “The SEC stated that was the majority of the questions that they had received during their consultation periods. They’ve offered consultations with issuers where they could call the Office of the Chief Accountant at the Division of Corporation Finance and request assistance or guidance on how they should be doing certain disclosures.”

Another company providing help with revenue recognition is Zuora, a San Jose, California-based business that hosted its annual Subscribed user conference in New York last week. Last year, Zuora acquired RevPro, which provides software for automating the revenue recognition process. Zuora and its RevPro unit work with three of the Big Four firms — PwC, Ernst Young and Deloitte — on helping clients implement the new revenue recognition standard, also known as ASC 606.

“In the last year or two, the demand for automation has been increasing and the partners really help us do all the work,” said Jagan Reddy, senior vice president for the RevPro product at Zuora. “The partners have built a fantastic practice around RevPro’s 606, so they can provide it to certain customers. When you do the revenue accounting, it’s not just implementing a tool. With 606, you have to make a lot of business process changes and system changes, so the partners have the expertise to drive all of that.”

Not only accounting firms and software vendors are getting requests for help with implementing the new revenue recognition standard. Peters of Intelligize noted that companies have been asking the SEC for help. In June, SEC Deputy Chief Accountant Sagar Teotia gave a speech in which he talked about the two primary subjects where the SEC received the most consultation requests: performance obligations and principal vs. agent guidance. That fits in with the comment letters the SEC has sent out to companies so far about their implementation of the new rev rec standard.

“We looked at about 32 early adopters, and of those about a third of those received substantive comments from the SEC regarding 606,’ said Peters. “We had identified about 18 different topics within 606 that the SEC had requested, and then of those entities three actually went through a second round of comments with the SEC, where the SEC had asked for additional information.”

Google’s parent company, Alphabet, was among those where the SEC was looking for extra details. “Alphabet was probably the most famous of those that came out,” said Peters. “Initially the SEC had five comments on the disclosure Alphabet did, and then they had followed it up with some comments that were focused on principal vs. agent disclosure that Alphabet had done and then also regarding the disaggregation of their advertising revenue. They were particularly interested in knowing why they felt they didn’t have to break out their advertising revenue by the different products.”

Alphabet responded that it looked at its online advertising as a whole, not by product or platform. “It’s all online advertising and that’s why they felt there was no reason to disaggregate the revenue at all,” said Peters. “Also receiving further comment requests was General Dynamics regarding why they had multiple contracts over the service life for various products, primarily in the defense industry, and why they hadn’t consolidated those into a single contract. General Dynamics came back and said, based on the guidance that was in 606, because the performance obligations that were required under those contracts weren’t entered into at or around the same time, they had to break them up into separate contracts. Then from 2018 we saw about 14 issuers that we had looked at and about 14 different topics for the 2018 year, very similar to what was focused on by the SEC.”

Even the public companies that have managed to implement the revenue recognition for this year are re-evaluating the approach they’re using, according to Zuora’s Reddy. “What we’re seeing is public companies have adopted 606 and they’re coming back and saying, ‘This is way too complex. I can’t do this, or I’m doing this manually today, but my compliance level is not so great because I can’t touch every transaction. I’m only touching my top 20 percent, and I don’t want to be in this scenario.’ Because two or three years down the line they may find a lot of discrepancies emerge and it might create a lot of audit risk.”

Many well-known public companies have yet to file their financial statements under the new standard because of their fiscal year-ends, and they too are likely to see comments from the SEC.

“You saw the early adopter wave, which was not very many, and then you saw the initial group of companies that were required to file with the 2018 date, and then upcoming is the late adopters, those companies that weren’t required to file because of the way the fiscal year was set up,” said Peters. “You have your Apples, Starbucks, people like that, are still going to be adopting it, probably by the end of this year or early next year. We still have that third wave of comments that will be coming through based on those, and we’re still seeing comments come through from the 2018 filers. That’s by no means done yet.”

Along with buying tools from companies like Zuora and Intelligize, many companies are also paying more fees to their auditing firms to make sure they’re handling revenue recognition correctly.

“One thing that we did notice, primarily from the proxies and the audit fee tables, is that a good amount of companies disclosed that they had an increase in their audit-related fees based on their implementation of 606,” said Peters.

Companies also turned to their accountants to help them decide whether to use the full retrospective or modified retrospective method of dealing with the new revenue recognition standard.

“They probably would have had to model whether they want to utilize the full retrospective vs. the modified retrospective, which one would probably be easier to implement from their end,” said Peters. “We’ve seen probably about 75 to 80 percent have chosen the modified retrospective, which is not surprising since it is the simpler method and also cheaper to implement.”

In some instances, companies are conditioning the bonuses paid to their CFO executives based on how they’re implementing the new standard, and encouraging their audit committee members to retire a little later.

“One other thing that was interesting that we noticed in the proxies was several companies disclosed that their bonus plans included the implementation of 606 as part of that for certain officers and directors,” said Peters. “One of the plans, for Adobe’s CFO, stated that implementation of 606 was part of the goals for that particular individual. Then one company actually waived their required retirement for directors. One of the directors who was actually chair of the audit committee was about to be required to retire because he had reached the age of 72, and they waived that so he could stay on to oversee the implementation of 606.”

He expects to see more companies keeping their accountants working past retirement age to help oversee the new revenue recognition, leasing and other accounting standards.

“When you think about just the transition itself, it would be difficult, especially with all this implementation, between 606 and then 842, you have pretty huge milestones to hit, particularly within consecutive years,” said Peters.

Companies will need to automate such processes with the help of the available technology and use them to report on not only how much revenue should be recognized for a given period, but also forecast how revenue will look in the future. “There are two aspects to revenue automation,” said Reddy. “One is about automating the day-to-day revenue operations, doing the accounting and compliance work and all that. The other side of automation is how to enable the finance team to forecast revenue. The CFO wants to know how they can look at all the transactions in the last six months or one year, and when they can expect the revenue. How is my revenue looking one year down the line?”