The American Institute of CPAs’ Financial Reporting Executive Committee is offering some draft guidance on various issues related to the implementation of the new credit losses standard.

The standard is also known as CECL because it uses a Current Expected Credit Loss model for estimating the allowances for expected losses over the life of a loan from a bank or other financial institution. It’s part of the financial instruments convergence project that the Financial Accounting Standards Board worked on with the International Accounting Standards Board, although the two standard-setters ultimately ended up diverging on their approach to credit losses. The AICPA guidance relates to the FASB standard for U.S. GAAP.

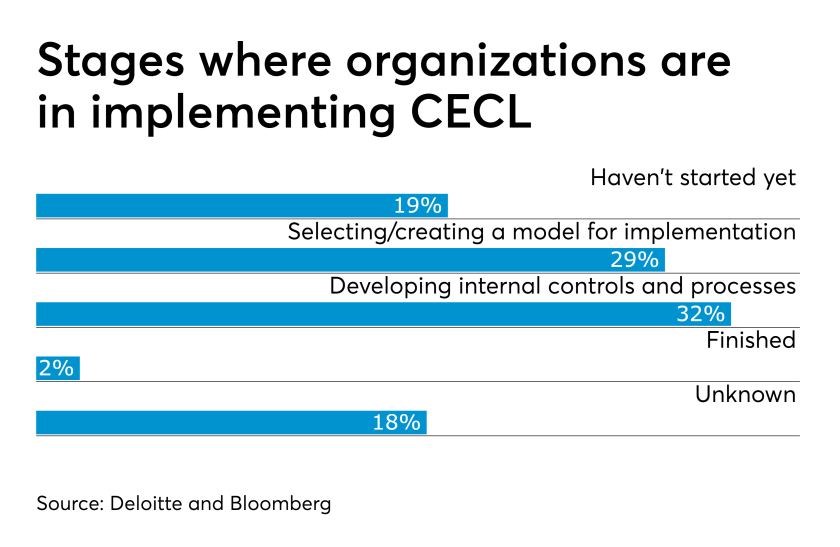

The CECL standard has proven difficult for many smaller banks and credit unions to implement, and FASB recently proposed to extend the deadline for the effective date of the CECL standard, along with several others, for private companies, nonprofits and smaller public companies, giving them an extra year to implement it (see FASB issues proposal to delay new standards).

The AICPA pointed out that the CECL standard is one of the most significant changes to financial institution accounting in 40 years, affecting the reserves for losses over loans booked and allowing for more forward-looking information to be considered when developing a best estimate. The AICPA’s Financial Reporting Executive Committee, also known as FinREC, issued four working drafts with proposed guidance describing a number of considerations that depository and lending institutions, along with insurance companies, should take into account:

“These issue papers demnstrate the AICPA’s continuing effort to ease implementation of the standard for auditors and their clients,” said Jason Brodmerkel, a CPA who is working with AICPA FinREC on accounting standards for depository and lending institutions. “It is a tremendous effort for our committee and the many volunteers on our task force all of whom are committed to help the financial reporting system adopt the standard.”

FinREC is asking for feedback on the implementation issues working drafts. They should be sent to Brodmerkel at Jason.Brodmerkel@aicpa-cima.com by Oct. 15, 2019.

When the drafts are finalized, they will be included in a new AICPA CECL AA guide.