The Internal Revenue Service needs to pay more attention to its employees’ side hustles, according to a new report.

The report, from the Treasury Inspector General for Tax Administration, found that as many as 2,200 IRS employees hold unapproved jobs outside the agency that put them at a higher risk of real or perceived conflicts of interest, and that 167 may have been doing work that is specifically prohibited — such as tax preparation.

Of those 167, 51 were working in accounting, 45 in legal services and 22 in tax, including five with income from tax prep chain HR Block.

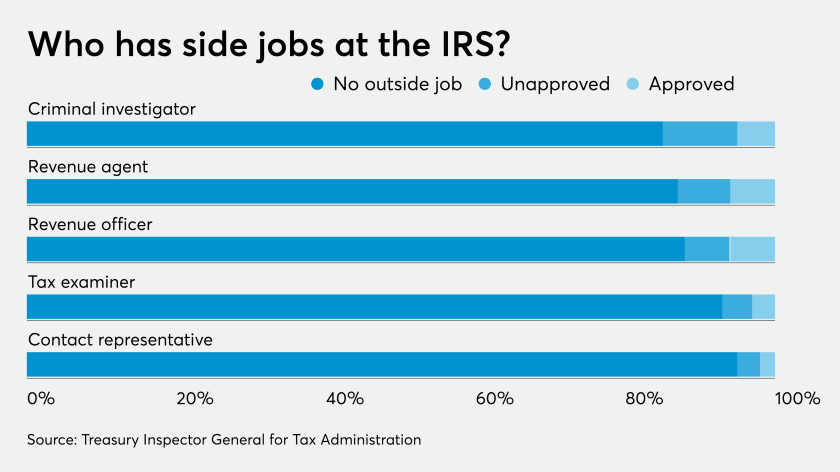

IRS criminal investigators were the most likely to have outside employment, with 15 percent holding second jobs, and two-thirds of those were unapproved, also the most of any IRS position. Revenue agents came in second, with 7 percent holding unapproved jobs, and a total of 13 percent holding outside jobs.

Perhaps more important, according to the report, is the fact that the IRS lacks adequate processes for tracking its employees’ other jobs and gauging their potential for conflicts of interest, and has no way to identify employees whose outside work is unapproved or prohibited.

Government employees are not necessarily forbidden from having outside employment, but those jobs must not present conflicts of interest with their government positions, and the employees must report them and get authorization to hold them through the Outside Employment System.

TIGTA conducted the audit that led to the current report because an earlier investigation revealed that as much as half of full-time IRS employees who had outside jobs did not have approval for them, or the jobs were not documented in the OES.

The OES alone does not guarantee that employees comply with the requirements around outside work, TIGTA noted; among other things, it found that two-thirds of the 14,155 employee requests in the OES in a sample period were not reviewed by managers on a timely basis — or were not reviewed at all.

TIGTA recommended that the director of the Workforce Relations Division review all the identified employees and address any conflicts; work with the Office of Chief Counsel to see if they need legislation to use tax data to identify potential conflicts; and better manage the OES, both in terms of requiring employee compliance and management review.

IRS management agreed or partially agreed with most of the recommendations, noting that it couldn’t commit to requiring some employees to using the OES without negotiating a change in work agreements.

Better at rehiring

In a separate report, TIGTA found that the IRS has improved its processes and procedures for rehiring former employees who had substantiated conduct or performance issues, but that the updated processes weren’t always followed.

Of 33 former IRS employees rehired during the sample period, the problem for 29 was one of failing to document the reasons for rehiring them, despite their previous issues. For the remaining four, the new guidelines were inappropriately applied.

TIGTA recommended that the IRS update its manual and tools to increase compliance with the new procedures and processes, train the appropriate officials in their use, and it conduct periodic quality reviews of hiring decisions.

IRS management agreed with all the recommendations.