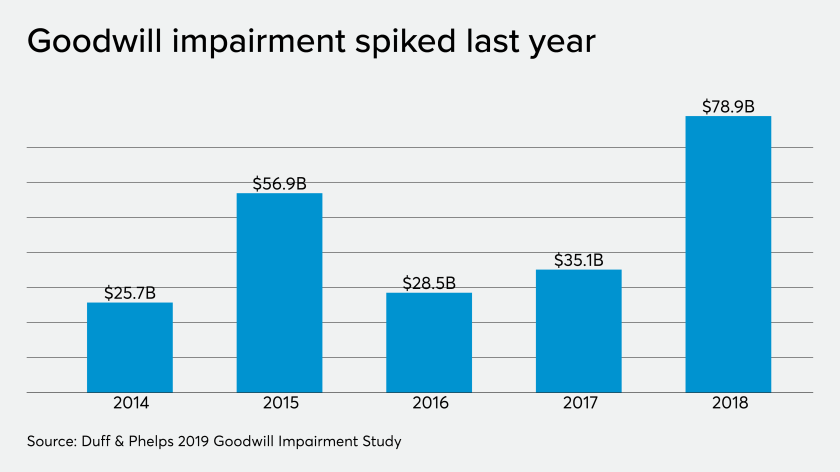

The total amount of goodwill impairment recorded by U.S. public companies reached $78.9 billion in 2018, up a staggering 125 percent from the prior year, according to a new report.

The 2019 U.S. Goodwill Impairment Study, released last week by Duff Phelps, examined the goodwill impairment trends of nearly 9,000 U.S. publicly traded companies from last year.

The study also found that MA activity also climbed to record high numbers, including a 16 percent increase in deal volume and 57 percent jump in deal value. That led to the highest level of goodwill added to the balance sheets of U.S. companies since at least 2008 when Duff Phelps began compiling the goodwill impairment reports.

The top 10 impairment events in 2018 accounted for nearly 70 percent of the aggregate impairment amount for the year. Seven out of 10 industries analyzed saw their aggregate GWI amounts increase for the second consecutive year. The industrials sector took the biggest hit last year, with an aggregate goodwill impairment of $25.1 billion, most of which ($22.1 billion) came from GE alone. The health care, consumer staples and energy sectors followed as the top three industries with the biggest increases in goodwill impairment.

The energy sector, which saw some relief in 2017 after three straight years as the most affected industry, found its improvement cut short thanks to the collapse of oil prices late last eyar.

Looking ahead to the likely figures in 2019, the top 5 goodwill impairment events disclosed to date reached a total of $24.5 billion, with several other significant impairments already being reported. Greg Franceschi, managing director and global leader of the Financial Reporting Valuation practice at Duff Phelps, predicted that while the full 2019 results for U.S. public companies won’t be known for several months, this is “an early indication that we may actually see a significant decrease in overall goodwill impairment this year.”

Duff Phelps’ 2019 study is being released at the same time the Financial Accounting Standards Board is exploring whether to change the accounting for identifiable intangible assets and goodwill. In July, FASB issued an Invitation to Comment on Identifiable Intangible Assets and Subsequent Accounting for Goodwill to explore whether cost-effective solutions that maintain or improve decision usefulness are feasible. FASB is in the process of reviewing the comment letters it has received and has asked for feedback through roundtable discussions to offer input into the board’s deliberations on these topics.

“Since issuing our Invitation to Comment last July, we’ve received about 100 comment letters,” said FASB Chairman Russell Golden at during a speech Tuesday at the AICPA Conference on Current SEC and PCAOB Developments in Washington, D.C. (see How accounting standards are like Ford v Ferrari). “And last month, 30 of those letter writers traveled all the way to Norwalk, Connecticut, to share their views on the topic at our public roundtables. Now, these numbers may not seem earth-shattering to you. But this level of interest at such an early stage of the process is striking. In this case, the staff ramped up communication among affected stakeholders. They employed targeted email campaigns, social media announcements, speaking engagements, and other communication vehicles to put this issue front and center. Based on the diverse views we heard at the roundtables, I expect an interesting public board discussion about intangible assets and goodwill early next year.”

Duff Phelps’ 2019 study on goodwill impairment takes an expanded look at the top 30 impairments recorded by companies in 2018, pointing to the factors noted in their SEC filings that contributed to the impairment. If FASB decides to change the accounting for goodwill impairment, the firm noted, such an analysis might not be possible in the future, limiting the kind of decision-useful information that would be available to investors.