Industry accountants see accounting software and online bookkeeping software as the technologies that will have the greatest impact on the profession in the next five years. Closely following these are data analytics and cloud solutions. Security, however, takes a back seat.

This data was compiled from a survey conducted by BlackLine, which attempted to find out how company finance departments globally interact with technology, and how they are handling security concerns surrounding customer and company data.

“Accounting tools that automate traditional mechanical processes, online bookkeeping, and other examples of cloud-based finance and accounting technology have been around for more than decade; but it takes time to penetrate the market and develop trust,” said Patrick Villanova, BlackLine’s principal accounting officer. “But you’re also seeing a new generation of financial analysts and accountants coming into the marketplace. They grew up with the internet and are both comfortable and accustomed to online systems and cloud-based software solutions. It’s intuitive to them, almost assumed or expected, that your accounting systems should be online, cloud-based and real-time. As these new members of the workforce advance their careers, you’re going to see an even more pervasive use of these tools in finance and accounting departments around the world.”

Newer, buzzier technology like artificial intelligence, robotics and blockchain were met with some skepticism, with a small minority of respondents seeing them actually impacting the profession in the near term. However, just about a third of respondents see cybersecurity solutions as one of the technologies having an impact, but that lukewarm attitude towards data security is troubling, Villanova said.

Ninety-seven percent of accountants agreed that data is “very valuable” to their business; however, 29 percent said their finance department, in order to increase the security of financial data, should rely entirely on the IT department to ensure utmost data security across the company’s network and systems. Only 25 percent of U.S. respondents said their finance department takes a highly proactive role in increasing the security of financial data, working with IT to make sure it pursues optimal data security.

“I was shocked at the numbers there,” Villanova said of the percentage of businesses that separate their finance department from security completely. “I would strongly advise against that. Finance and accounting leaders of a company have a fiduciary responsibility to ensure client data is protected. I would never completely outsource that to another department. You should have a highly proactive role in this process. Yes, IT are the experts, but you should be communicating regularly with them in terms of [putting] protocols in place to safeguard your data and assets.”

Accounting and bookkeeping software, variants of which have been in use for decades, are tools accountants see as within their domain. They perform accounting tasks, which accountants are trained in. Analytics and automation give accountants the opportunity to offer their clients value-added services, moving them into advisory roles. Security, however, feels like the IT professional’s domain because accountants believe they are not trained in it as they are in the tasks of their profession.

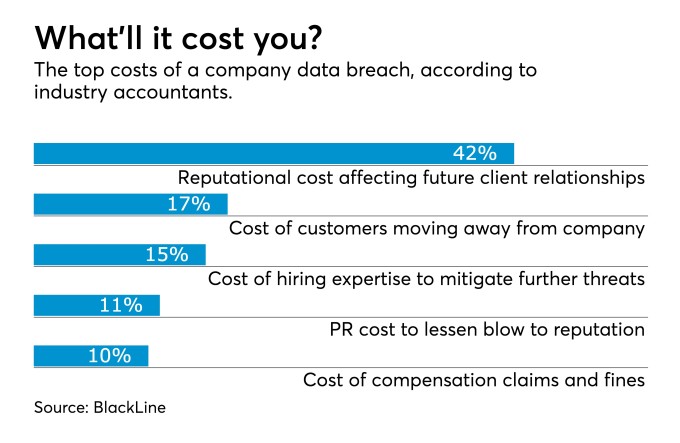

While CFOs, controllers or company accountants may feel they’re not qualified to take a more active role in security at their company, they understand the cost of a data breach: 42 percent of respondents to the survey think the greatest loss would be the reputational cost that might affect future customer relationships. Other top concerns were the cost of customers potentially moving away from the company (17 percent), the cost of hiring expertise to help mitigate any further threats (15 percent), and the cost of potential compensation claims and fines (10 percent).

“I think the age of cloud-based, real-time accounting software and controls systems will only enhance the security of your financial assets,” Villanova explained. “The basis for that argument is when any kind of a crime has been committed, the biggest thing working against the victim is the elapsing of time. This is true with cybercrime as well because if you’re running on antiquated systems that are not online and real-time, precious time is lost between the incident and the moment of discovery. Hopefully a breach doesn’t happen, but if it does, having that 24/7 transparency at your fingertips will help you identify the issue much faster than you would without it.”

BlackLine’s survey was conducted by Censuswide and included 900 CFOs, finance directors and accountants around the world in large and midsized businesses.