One of the most challenging and stressful tax seasons in recent memory is behind you. I hope you’re making time for some RR and doing a little self-reflection. That’s what I do when I’m surfing near my home in Southern California. No matter when I go out on the water or what the conditions are, the same few surfers seem to be catching a vast majority of the waves. It never fails. The wave masters are not all young professional surfers. They don’t necessarily have better technique or better boards than the rest of us. They just have a knack for putting themselves in the best possible position to catch the best waves at the best time.

The same thing happens year after year in the accounting profession. Our research shows that only a tiny fraction of the CPAs who run their own firms or who rise to the level of partner will consistently earn $1 million a year (see my earlier articles, Lessons from millionaire accounting partners and More lessons from millionaire accounting partners). Millionaire CPAs can be found at firms of all sizes, by the way, not just at the Big Four or Top 100.

What makes these ultra-high performers different from the rest of the profession? Do they have superhuman stamina, exceptional intelligence or superb technical competence? Not necessarily. What they do have is a set of unique skills and attributes that aren’t taught in business schools or CPE programs. Here are three that stand out to me:

1. They are highly attuned to the human element.

2. They are committed to thought leadership.

3. They think beyond hourly billing.

Let’s take a closer look at each:

1. Importance of the human element

The highest-performing CPAs tend to have high EQ (emotional intelligence). Some are born with EQ; others work hard to develop it. But high-performing CPAs really know how to connect with their clients and the people around them. They ask clients lots of questions about their businesses. They ask lots of questions about their families. They ask lots of questions about what’s important to them. They ask lots of probing questions that other people, including their advisors, have never asked them before. This type of questioning — accompanied by deep listening — accomplishes several important things:

a. It builds rapport with your client.

b. It cements your position as the most trusted advisor in their life.

c. It drives opportunities for more projects and high-margin fees at your firm. I’ll talk more about billing in a minute.

All too often, advisors (CPAs, attorneys and insurance pros) go into a client situation and think they know everything about the client and how they’re going to solve the client’s problem. That’s short-sighted. Instead, you should borrow a page from the ancient Greek philosopher Socrates and approach every situation or encounter as though you don’t know anything at first. Socrates knew the only way to gain clarity and arrive at an answer was to keep asking deeper and deeper questions. The Socratic method still works well today.

At your next meeting with a client or prospect, try spending 90 percent of the meeting asking questions, rather than rattling off regs, facts and stats. You’ll be surprised by the connection you develop with your client and by the opportunities you unlock.

Jason Trenton, a top trust and estate attorney in the Los Angeles office of Venable LLP’s Tax and Wealth Planning Practice, told me recently that a large part of his firm’s success comes from forging a deep understanding of clients, including their family relationships and what’s important to them beyond money. “Where I see other advisors fall short, and sometimes I can be guilty of this, is getting too buried in technicalities and minutiae,” said Trenton. “That’s not where clients focus.”

According to Trenton, good advisors ask clients the right questions to determine everything they want, not just tax-driven solutions. “My job is then to overlay clients’ desires with our technical capabilities as opposed to leading with those,” he added. “This process creates the ideal plan that will deliver everything clients want.”

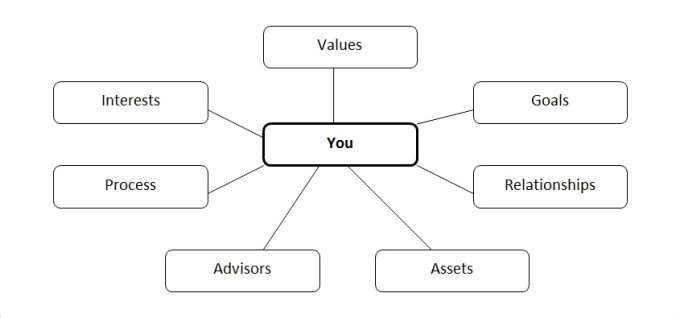

Mind Map

You will probably find yourself with a ton of notes and material to sift through. After I have an in-depth meeting with a client, I immediately create a “Mind Map” so I can visually record all the data I have collected. Don’t put off this exercise for later.

Source: Liquidity You: A Personal Guide for Tech and Business Entrepreneurs Approaching an Exit, 2017

Before sharing the map with my client or my team, however, I take some time to reflect on what I now know about the client, how I can add value to the relationship and how I can really help them. Quite simply, our job as advisors is to make sure we get clients what they want. Our job is not to tell them what they need or tell them what they need to do.

Feel free to reach out to us for more information about Mind Mapping a client intake interview info@agassetadvisory.com.

2. Commitment to Thought Leadership

According to AES Nation research, almost all millionaire CPAs (96 percent) are actively working toward being thought leaders. By comparison, just three in 10 (29 percent) lower-earning CPAs are working to become thought leaders. It’s easy to call yourself a thought leader, no matter what your profession is. But, if you’re truly a thought leader, then your prospective clients, your current clients, your competitors and industry watchers recognize you as the “go-to” person in your niche. You should be the name that people drop. When you are truly a thought leader based on the definition above, then you are able to profit greatly from that positioning.

Becoming a thought leader

If you’re looking for a secret formula or special trick, there isn’t one. It’s pretty simple: Write, speak and seek out media coverage. It’s going to take some work, but I don’t know of a single millionaire CPA who says the effort isn’t worth the time.

In the chart below, you can see how firms that are expecting strong growth are more likely than their less optimistic peers to find value in speaking, publishing and media coverage. You’ll also see how firms expecting flat or declining growth are more likely to rely on social media and other tactics that don’t require as much time, thought or mental heavy lifting.

Percentage of firms considering selected Thought Leadership tactics “very” or “extremely useful”:

Sources: CPA Trendlines, The Financial Awareness Foundation and HB Publishing Marketing Company LLC, 2019

Sure, writing, speaking and working the press take some time and effort. To make the process a little less daunting and time efficient, you can collaborate with other CPAs, attorneys and advisors in your niche to help you develop thought leadership material and spread out the workload. Collaborating with other professionals on an article or presentation is a lot like working on a client case together. It keeps you on task. It provides a wider perspective and it makes the process of authoring and presenting more enjoyable and a lot more applicable. You can reach out to us if you would like more information about thought leadership collaboration at info@agassetadvisory.com.

3. Beyond hourly billing

Clients know you are a highly skilled and highly competent professional. They don’t care how long it takes you and your team to handle their taxes or other difficult financial issue for them. They just want you to make it go ways. Instead of hourly billing, millionaire CPAs tend to use project-based fees—fixed fees based on the complexity of the work and the value delivered to the client, not on how long it took you to do it.

Example: I recently asked a CPA what he would charge to do a certain kind of detailed financial analysis. When I asked how he arrived at his number, he told me his firm estimated that it would take “X” number of hours to complete the report. Based on each partner and associate’s hourly rate, times the number of projected hours, that’s how he came up with the number.

Then I asked if he factored in the actual value of the deliverable his firm was delivering to the client. Not surprisingly, he said no. I suggested that he seriously reconsider how he came up with project-based fees. For instance, if you have a method for saving a client hundreds of thousands of dollars in taxes, it’s going to require you and your team to put in some work and possibly enlist outside professionals. You should be compensated for that in a project-based fee for the value you are delivering. I’m not suggesting you charge a percentage of the tax savings you achieved for your client—that’s unethical. Rather, it’s about taking a step back and saying, “What have we done here and what’s the value being delivered? What’s a reasonable and appropriate fee to charge for this?”

By the way, when you approach billing this way, your clients are going to be a lot happier about the transparency and simplified (no-surprise) billing. You won’t be wasting their time with annoying statements or emails showing fractions of hours for what you are billing. Meanwhile, clients won’t be scratching their heads wondering why they’re paying you.

Venable’s Trenton said most of his clients prefer project-based fees to hourly billing because project-based fees provide “transparency and certainty. Clients have a much better understanding of what they get for what they are paying for,” he added.

Ask your clients and prospects a lot of questions so you can deeply understand their goals and what makes them tick. Work to become a thought leader in your niche and charge clients based on the value you’re providing them, not on how long it took you and your team to work your magic. You’ll be glad you did.

For reprint and licensing requests for this article, click here.