The six largest credit card issuers have set aside billions of dollars worth of reserves in response to the novel coronavirus as well as the adoption of the Financial Accounting Standards Board’s new credit losses standard.

A report released last Friday by Moody’s Investors service examined how much American Express, Bank of America, Capital One Financial, Citigroup, Discover Financial Services and JPMorgan Chase are putting aside for the new accounting standard, also referred to as CECL for the Current Expected Credit Losses model it follows, in addition to the COVID-19 pandemic.

All the top banks have been confronting the challenge amid the pandemic of estimating future losses along with the effectiveness of government support programs during this time of uncertainty, giving rise to comparability issues across firms. Nevertheless, all six banks have substantially increased their reserves, which Moody’s views as a positive for their bondholders.

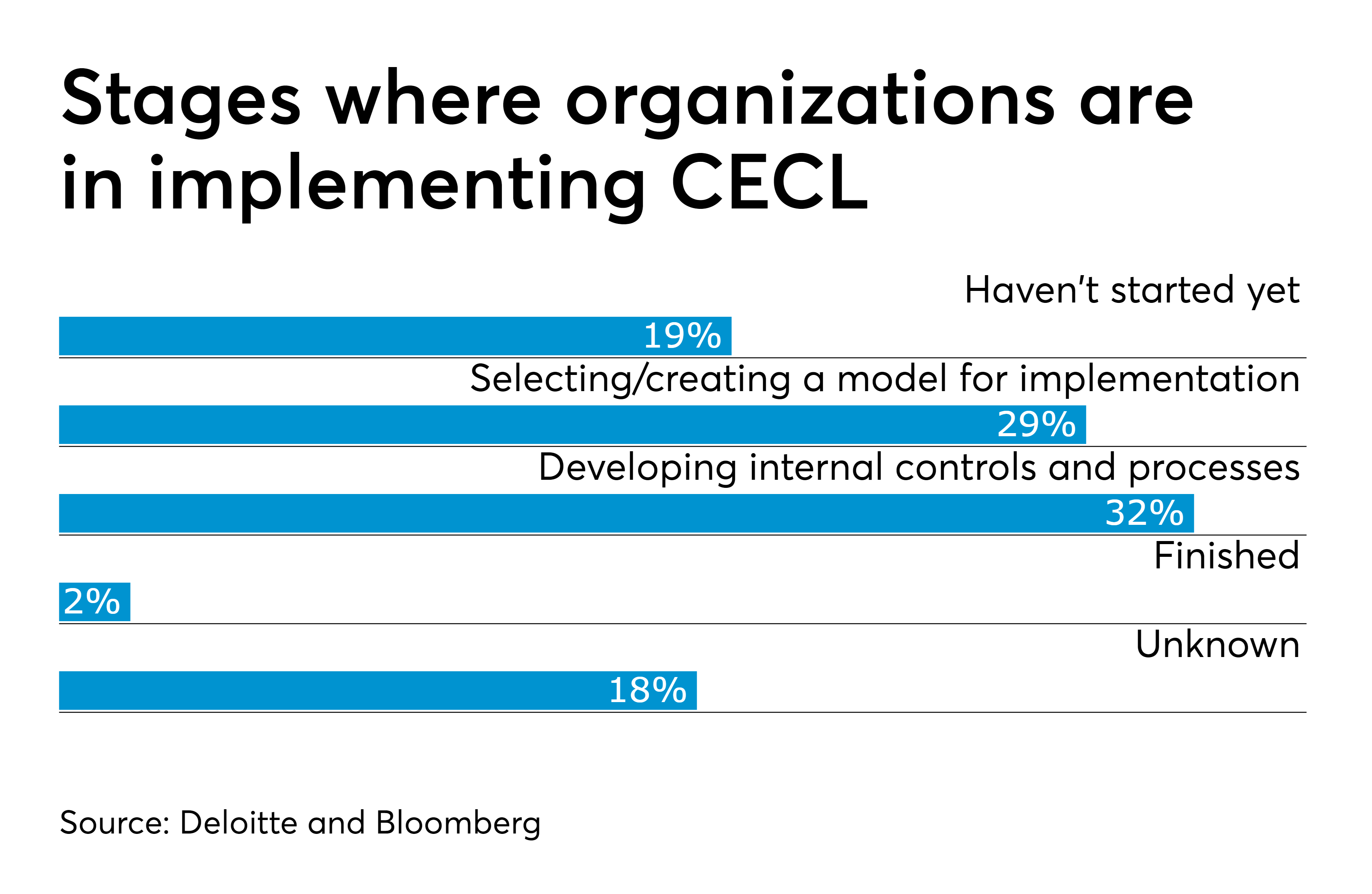

The CECL standard has added extra complications along with the economic fallout from the coronavirus, which has made it difficult for many consumers to pay their credit card bills. CECL took effect for the large publicly traded companies in January before the pandemic began spreading across the U.S., but as part of its efforts to provide some relief from the impact of COVID-19, FASB voted to defer the effective date of CECL and several of its other standards for private companies, smaller reporting companies and nonprofits, giving extra time to credit unions and small banks to get ready for the new standard. Last year, FASB also extended the timelines for CECL and several other standards (see story). The Senate also included a provision to give banks extra time to implement CECL in the CARES Act in response to the pandemic (see story). Several banking regulators, including the Federal Reserve, the Federal Deposit Insurance Corporation and the Office of the Comptroller of the Currency, also provided relief on regulatory capital requirements for CECL in March.

Nevertheless, the combined impact of the coronavirus and the CECL standard are putting pressure on banks, according to the Moody’s report. “The reserve builds have sharply reduced profitability at the banks, which have all also stopped share repurchases,” said the report. Each bank has faced the challenge of estimating future losses as well as the effectiveness of government support programs during this time of uncertainty, giving rise to comparability issues across firms. Nonetheless, all six firms have substantially increased reserves, which is positive for their bondholders.”

The report noted that a big part of the reserve build at the six banks is driven by their exposure to credit cards, which typically have higher charge-offs than most other types of bank loans. The longer average loan life is also driving higher than average CECL loss reserves for credit cards. The average allowance for credit card loan losses for the six biggest credit card banks in the U.S. has almost tripled from just under 4.0 percent of credit card loans outstanding as of the end of 2019 to just under 11 percent as of the end of the second quarter of 2020.

Financial analysts can help ferret out these detailed comparisons and highlight them. Otherwise, investors may need to seek out information on their own in some cases about the impact of the pandemic and accounting standards on financial reporting, according to one expert. “If companies don’t give you things, you need to ask questions as an investor to understand,” Sandy Peters, head of financial reporting policy at CFA Institute, told Accounting Today. “They obviously have a view and they have built that view into estimates for impairment testing, allowance for credit losses and the like, so they have some view of the future, but are they telling you that view more explicitly, or are they just embedding it in the measurements that are included in their financial statements that you have to decode?”